Welcome to this edition of Potato 2.0. Today, we are analyzing a global landscape defined by a sharp contrast between European oversupply and American strategic expansion. While some regions are struggling with price collapses, others are capitalizing on currency fluctuations and new trade agreements to redefine the market.

https://open.spotify.com/episode/03zF1pulxqhOoSYnFPrh54?si=8lkwzkP4R6iHnn9_Ljt6ig

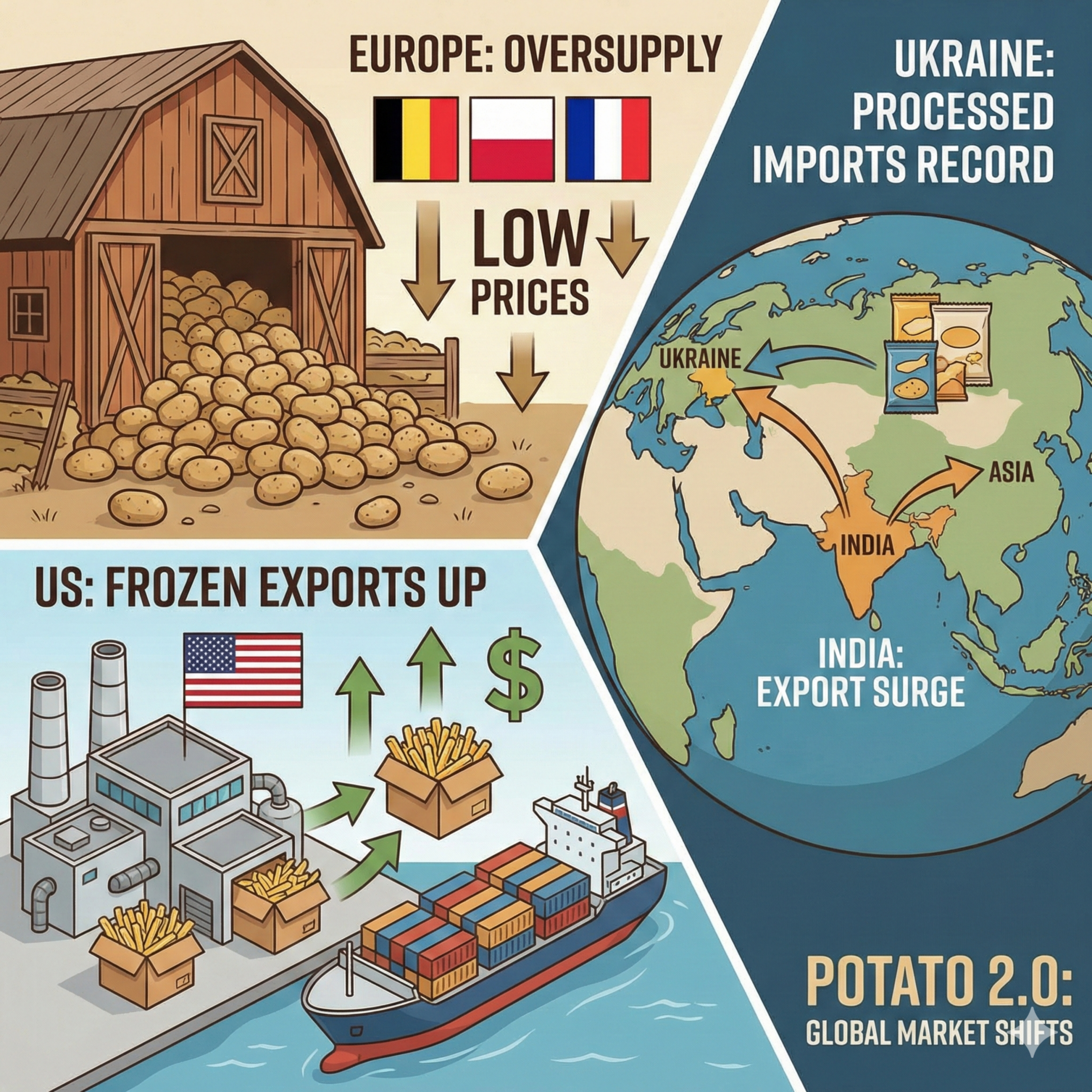

The European Glut: Record Lows in the West and East

The European potato sector is currently navigating a period of significant volatility. An excess of supply has hit the markets in Belgium, Poland, and France particularly hard. This surplus has driven prices down to record lows, creating a challenging environment for producers.

The abundance of raw material has overwhelmed local demand, forcing growers to rely heavily on industrial processing. However, even with factories running at high capacity, the sheer volume of the harvest continues to suppress market value across these key agrarian hubs.

US Dominance: The Weak Dollar and the Frozen Fry Surge

In stark contrast to the European struggle, the United States has solidified its leadership in the frozen potato product segment. A primary catalyst for this growth has been the weakening of the U.S. dollar, which has made American exports significantly more competitive on the global stage.

The U.S. has leveraged this advantage to expand its footprint in the high-value frozen fry market. By offering more attractive pricing than its international competitors, American suppliers are capturing a larger share of the global fast-food and retail sectors.

Asian Dynamics: India’s Ambition and Ukraine’s Import Peak

The trade landscape in Asia and Eastern Europe is showing remarkable new trends.

- India’s Export Surge: India has dramatically increased its export volumes, moving beyond local supply to become a major player in regional trade. Their ability to scale production and meet international quality standards is reshaping supply chains across the continent.

- Ukraine’s Processed Record: In a surprising turn, Ukraine has hit an all-time high for the import of processed potato products. This indicates a significant shift in domestic consumer behavior, where the demand for ready-to-eat or easy-to-prepare products is outstripping the capacity of local processing facilities.

Trade Barriers and Regulatory Breakthroughs

The geopolitical side of the potato trade is equally active. A major development is the expansion of phytosanitary permits for American suppliers in South Korea. This regulatory shift, combined with the strategic management of U.S. customs duties, has paved the way for a more seamless flow of American goods into the Korean market.

These administrative victories are crucial for maintaining long-term market stability and ensuring that supply can meet the growing demand in high-tech Asian economies.

Data Analysis: Consumer Demand and Stock Levels

Statistical data from the world’s largest agricultural regions confirms a fundamental shift in the industry. We are seeing a global move toward “value-added” products. While raw potato stocks are high in Europe, the inventory for processed goods is moving much faster.

Current warehouse data suggests that while the volume of potatoes is high, the “profitability” is migrating toward companies that can transform the raw tuber into a branded, processed commodity. Understanding these inventory levels is key to predicting price movements in the coming fiscal quarters.

Potato 2.0 Summary: The global market is no longer just about who grows the most; it is about who can process, export, and navigate trade regulations most effectively. The “Potato 2.0” era is defined by the frozen fry, the exchange rate, and the ability to pivot to emerging markets like South Korea and India.